How high will the RBA’s cash rate get and how quickly? That’s one of the questions at the forefront of many people in the property development’s minds.

With five consecutive rate hikes totalling 225bps, the RBA has moved at an unprecedented and record pace to combat spiralling inflation. RBA governor, Philip Lowe, now expects inflation to peak later this year around 7.75%. But that’s little more than an educated guess at this stage and the environment remains unpredictable. Some will recall that throughout most of 2021, Lowe maintained that rate would not rise until 2024.

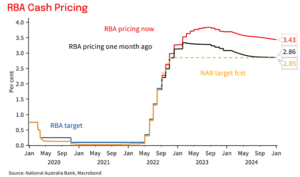

National Australia Bank’s dovish rate forecast. Source: NAB

There is a divergence in opinion as to the pace and quantum of the RBA’s rate moves amongst the economists of some of Australia’s largest banks. Perhaps the most dovish is NAB’s Tapas Strickland who, post September’s RBA hike, gave an update suggesting that the cash rate peaks at 2.85% with the next rate rises being 25bps. At the other end of the spectrum sits Westpac’s Bill Evans who today predicted a further 50bp hike next month and sees rates not levelling out until 3.60%.

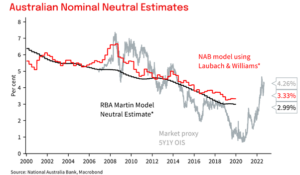

Neutral Cash Rate Estimates. Source NAB

NAB’s dovish stance is partially a result of where they model ‘neutral’ rates for Australia. Whilst Bill Evans believes that the RBA is currently more focussed on controlling inflation and may overshoot ‘neutral’ in the short to medium term as a result.

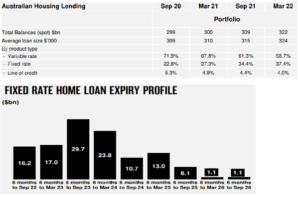

Australian fixed rate mortgage data. Source: NAB

BPFM’s view? We are at the Hawkish end of the spectrum in the short term, seeing rates continue the upwards trajectory until the end of the year. As at March 2022, 37.4% of Australian mortgages were on a fixed rate. The impact of the RBA’s rate increases will therefore not be felt immediately by a significant percentage of Australian homeowners. However, by the end of 2023, 70% of these fixed rates will have expired and the full impact of the RBA’s rate hikes will be felt. The RBA will want to ensure that inflation is under control before any reversal in rate policy. However, with the delayed deflationary impact of the policy caused by fixed rate mortgages, it is possible that the RBA will overshoot and we will see rates ease slightly mid next year.